Trending

CHARLESTON -- Legislation passed toward the end of the 2021 regular session was supposed to fix constitutional issues with the way West Virginia assesses the value of property with natural gas production.

Instead, no one is happy with the new rules.

Lawmakers passed House Bill 2581 in April over the objections of several Northern Panhandle and North Central West Virginia elected leaders. The bill required the State Tax Commissioner to develop a revised methodology to value oil and natural gas properties.

The State Tax Department submitted an emergency rule over the summer for how it planned to carry out HB 2581, though the Legislature's Rule-Making Review Committee has yet to take up the final rule. But Marshall County Assessor Eric Buzzard hopes lawmakers can scrap the rule and start over during the 2022 legislative session.

"I think the people are just going to be paying entirely too much money, and ultimately is going to be giving the big businesses a break and that's not the business I'm in. I'm in the business of taking care of our county residents," Buzzard said. "Hopefully once session gets in they'll evaluate it and it will be beneficial to county residents more than out-of-state oil and gas companies."

According to the emergency rule, the value of oil and natural gas-producing property is determined by applying a yield capitalization model based on a weighted average cost of capital to the net receipts (once royalties and annual operating costs are subtracted from gross receipts) for working interest, with a yield capitalization model applied to gross royalty payments for royalty interest.

"The key methodology changes have been a statutory move to actual receipts less costs … the new capitalization rate that is now derived using a weighted average cost capital approach which we believe is a more accurate representation of the actual cost of employing capital in the investment and more likely captures the risk," said Erin Winter, acting deputy tax commissioner, during a legislative interim meeting in September.

The State Tax Department also eliminated the provision that called for the 18 months of decline from the discounted cashflow analysis, and natural gas liquids -- along with the value reduction costs to make it marketable -- are included as a value item.

What does any of that mean? That's a question that major natural gas producers, accountants, and county assessors would like to know.

"I don't get their thinking on it," Buzzard said. "I don't think anyone does and nobody knows what is going on."

Buzzard said the rule is far too complicated and there has been little education from the State Tax Department for county assessors or even the public at large going into the next tax year.

"The residents have not been educated enough about this system and neither have assessors up to this point," Buzzard said. "It used to be based on a three-year average of producing. Now they're going by actual costs. It seems like it will benefit the big natural gas and oil companies than our county residents. An average over three years is a more realistic value when it comes to paying your taxes than your actual producing amount."

One of the biggest supporters of HB 2581, the Gas and Oil Association of West Virginia, believed the bill would help simplify natural gas property assessments. Instead, they say that the State Tax Department's emergency rule gives the state more power than the bill intended. As a result, state tax officials made a simple change more complicated.

"(House Bill) 2581 was a simple bill … if you look at the emergency rule that was passed, it's not very simple at all," said Mark Monteleone, co-chairman of the tax committee for the Gas and Oil Association of West Virginia (GOWV), to lawmakers in September. "It's a very complex rule that goes beyond, we believe, the scope of the statute. For that reason, we believe they have exceeded statutory authority of 2581."

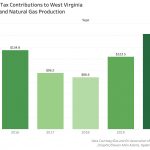

According to GOWV, natural gas production in West Virginia increased by 14 percent between 2019 and 2020, with property tax contributions increasing by more than 24 percent over 2019 numbers. Natural gas production in the state increased from 1.4 trillion cubic feet in 2016 to 2.5 billion trillion cubic feet in 2020. During that same time, property tax contributions increased from$134.8 million to $162.7 million.

The version of HB 2581 passed by the House of Delegates created a formula to value oil and natural gas property by using a weighted average price from regional markets, less the actual expenses as reported by the taxpayer. It was the state Senate who stripped out that formula and left it up to the State Tax Department to develop a formulation that the Legislature could approve through its rule-making review authority.

The previous methodology used for determining the value of natural gas-producing property was thrown out by the West Virginia Supreme Court of Appeals in 2019 in Steager v. Consol Energy Inc, requiring lawmakers to pass HB 2581.

"… The Court noted that the legislative rule for the valuation of producing natural gas wells did not address gathering, compressing, processing, and transportation expenses, and that the Tax Department's determination that such expenses are not 'directly related' to the 'maintenance and production' of natural gas was not arbitrary, capricious, or manifestly contrary to the enabling taxation statute," according to an analysis by Craig Griffith, an attorney with Frost Todd Brown law firm in Charleston.

Speaking to lawmakers in September, Winter said the State Tax Department was willing to work with taxpayers and county assessors to implement the new rule.

"Going forward, we will continue to review tax returns to the extent that we have the resources to do so," Winter said. "We think reasonableness as the starting point of any inquiry into the actual costs is the most workable solution for us.

"And the Tax Department will continue to work with industry moving forward to ensure completeness and accuracy and make sure the actual value is determined, and we will work with the counties to ensure compliance by the industry."

However, county tax officials have felt left out of the entire process, from the drafting of HB 2581 to the release of the emergency rule from the State Tax Department last summer. While the State Tax Department develops the rules, it's up to county assessors to determine the actual values using the new rule.

The original version of the bill would have resulted in a $9.1 million property tax revenue loss to county governments and county school systems.

Eight counties in the Northern Panhandle and North Central West Virginia would have taken a $7 million hit under the previous plan. It's unclear how much of a hit the state and natural gas-producing counties would take under the new rule.

"We have not received anything," Buzzard said. "We've been requesting it for months and we have not received any totals. Of course, we always hear it's going to be minimal, but minimal for a gas-producing county is substantial.